Complete SEO and Blogging Guide in 2024 for Ecommerce and...

Parcel Monitor: Top Logistics Carriers Dominating the U.S. Market...

The Supply Chain of White Label Products: Make It Work...

White Label vs Private Label: Choosing the Right Manufacturing Method ...

How to Navigate White-Label Manufacturing & Its Economics as an...

Trending Products 2024: White Label Products to Sell...

Understanding Hyper-Personalization...

The Ultimate Guide for DTC Brands in 2024...

European e-commerce is booming with a forecasted CAGR of 8,91% ...

Unlocking the Power of Private Label Health and Wellness Tinctures:...

The Evolution of Private Label Food Products: From Generic to...

Parcel Monitor: Top Retail & E-Commerce Trends for 2024 and...

NY Chamber LIAACC Tells Why Joining A Chamber of Commerce...

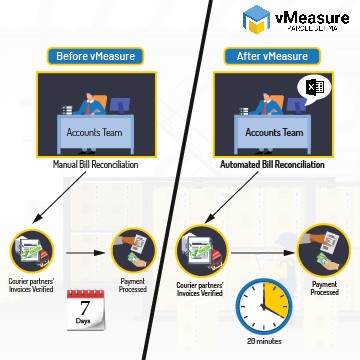

Beyond Dimensioning: How vMeasure Changed Parcel Measurements and Finance Together ...

The Private Label Sector Surges in 2024...

Exploring Modern eCommerce Trends: Dynamics Shaping Online Selling in 2024 ...

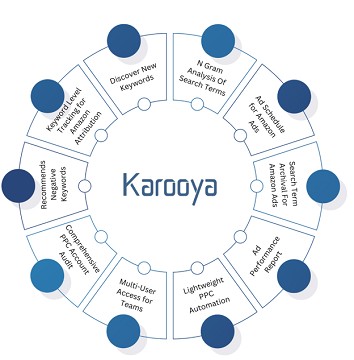

Karooya: Maximize Your Online Reach and Grow Your Business With...

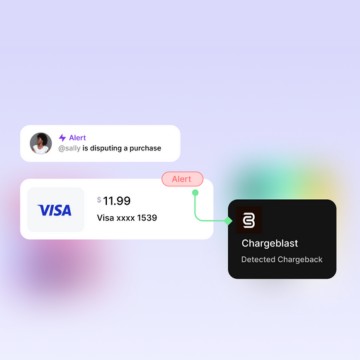

How Chargeblast reduced our chargeback rate by 98%...

White Label Trade Show Returns to New York...

Introducing White Label World Expo...

Vitamin and Supplement Contract Manufacturer NutraPak USA Moves into New...

White Label World Expo returns to NYC!...

Private Label Industry Award Winner!...

CBD & Hemp Wholesaler of the Year Award Winner!...

Leading Manufacturer Award Winner!...

Service of the Year Award Winner!...

Innovative Product of the Year Award Winner!...

Global Influencer: Travels By Sunny...

Work''n''roll: Special Show Offer!...

CBD & Hemp Wholesale World is Around the Corner!...

1

2